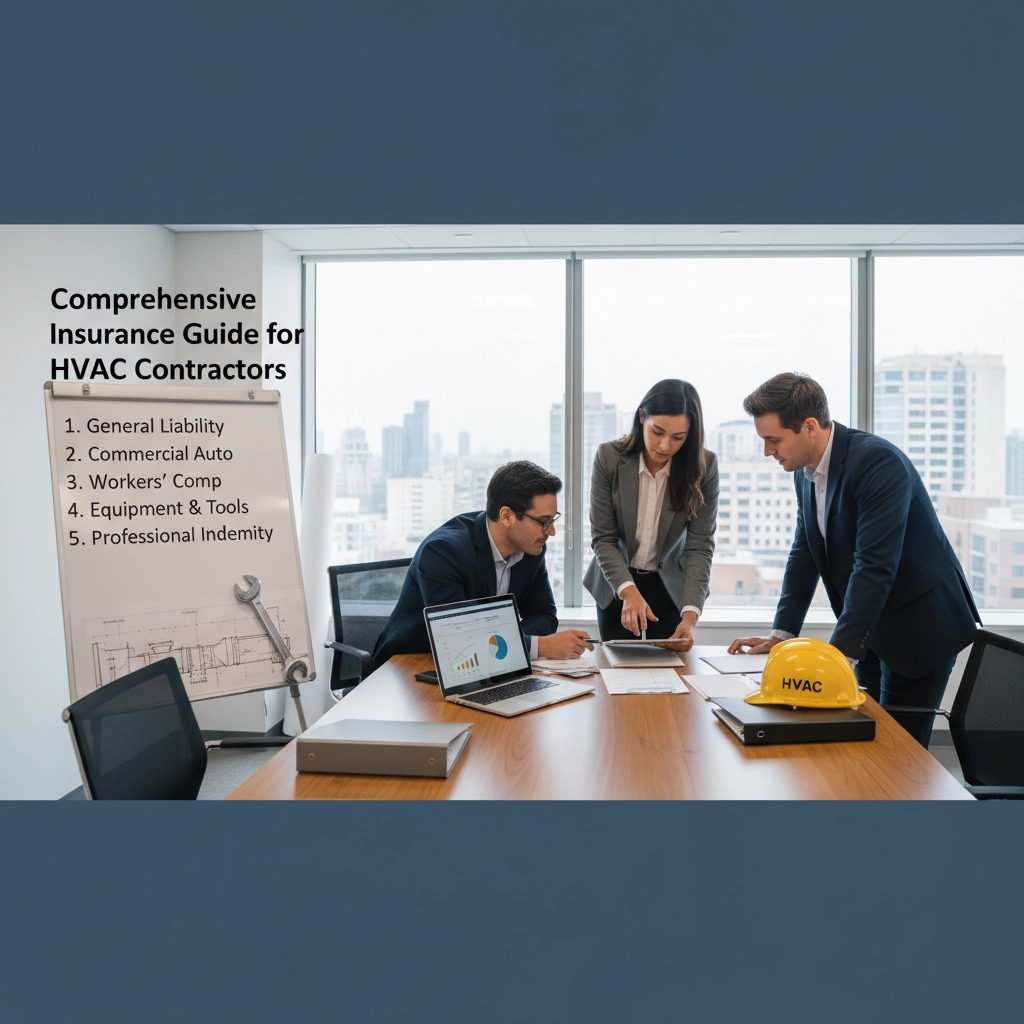

Comprehensive Insurance Guide for HVAC Contractors

- marketing676641

- Nov 27, 2025

- 42 min read

HVAC contractors face unique risks every day. You work with refrigerants, electrical systems, and heavy equipment. You climb rooftops, crawl through basements, and handle hazardous materials. One mistake can result in property damage, injuries, or environmental contamination. The right insurance coverage protects your business from these risks and helps you meet licensing requirements.

Essential Coverage Types for HVAC Contractors

General Liability Insurance

General liability insurance forms the foundation of your insurance program. This coverage protects your business when your work causes property damage or bodily injury to third parties. Common scenarios include damaging a customer's flooring while moving equipment, causing water damage from a faulty installation, or a client slipping over your tools.

The policy includes completed operations coverage. This protection extends beyond the job site and covers claims that arise after you complete the work. A furnace malfunction six months after installation that causes water damage falls under completed operations coverage.

Product liability coverage is included in general liability policies. This protection covers claims related to defective equipment you install or products you sell to customers.

Workers' Compensation Insurance

Workers' compensation insurance is mandatory if you employ technicians or administrative staff. HVAC work involves physical demands that increase injury risks. Technicians lift heavy equipment, work in cramped spaces, and handle electrical components.

This coverage pays medical expenses and lost wages for employees injured on the job. Workers' compensation also protects your business from employee lawsuits related to workplace injuries. Most states require this coverage for businesses with employees.

Commercial Auto Insurance

Your work vehicles and equipment need commercial auto coverage. Personal auto policies exclude business use and commercial equipment. Commercial auto insurance covers your vans, trucks, and trailers used for business purposes.

The policy includes liability coverage for accidents involving your vehicles. Physical damage coverage protects against theft, vandalism, and collision damage. Commercial auto policies also cover tools and equipment stored in vehicles up to specified limits.

Tools and Equipment Coverage

Tools and equipment coverage protects your valuable assets against theft and damage. This coverage, also called inland marine insurance, follows your tools whether they're at the job site, in your vehicle, or at your shop.

Standard property insurance typically excludes tools and equipment used away from your business premises. Specialized tools and equipment coverage fills this gap. The policy covers diagnostic equipment, hand tools, power tools, and specialized HVAC instruments.

Professional Liability Insurance

Professional liability insurance covers claims related to your professional advice and services. HVAC contractors increasingly provide consulting on energy efficiency, indoor air quality, and system design. Professional liability protects against claims of negligence, errors, or omissions in these services.

This coverage applies when customers claim your system design was inadequate, your recommendations were wrong, or your work failed to meet professional standards. Professional liability insurance covers legal defense costs and damages awarded against your business.

Pollution Liability Insurance

Standard general liability policies exclude pollution-related incidents. HVAC contractors work with refrigerants, oils, and chemicals that can cause environmental damage. Pollution liability insurance specifically covers these exposures.

The policy protects against costs from refrigerant leaks, contamination from system failures, and regulatory fines. Environmental cleanup expenses can reach thousands of dollars. Pollution liability coverage provides essential protection for these risks.

Specialized Coverage Options

Cyber Liability Insurance

Modern HVAC businesses rely on digital systems for scheduling, billing, and customer management. Cyber liability insurance protects against data breaches, ransomware attacks, and system failures. The coverage includes notification costs, credit monitoring services, and business interruption losses.

Umbrella Insurance

Umbrella insurance provides additional liability coverage above your primary policies. Large commercial projects may require higher liability limits than standard policies provide. Umbrella coverage extends your protection without purchasing separate high-limit policies.

Surety Bonds

Many jurisdictions require surety bonds for HVAC contractor licensing. Bonds guarantee you will complete work according to contract terms. Unlike insurance, bonds protect project owners rather than your business. However, bonds demonstrate financial responsibility to customers and regulatory agencies.

Coverage Requirements and Compliance

Licensing Requirements

HVAC contractor licenses typically require minimum insurance coverage. General liability insurance is standard for most licensing authorities. Workers' compensation insurance is required if you employ technicians. Verify specific requirements with your local licensing board.

EPA Certification

EPA certification is mandatory for technicians handling refrigerants. Proper certification demonstrates compliance with federal regulations and helps prevent costly violations. Insurance carriers may require EPA certification for pollution liability coverage.

Customer Requirements

Commercial customers often specify minimum insurance requirements in contracts. Common requirements include specific liability limits, additional insured endorsements, and waiver of subrogation clauses. Review customer requirements before bidding projects.

Business Owner's Policy Benefits

A Business Owner's Policy (BOP) combines general liability and commercial property coverage in one package. BOPs typically cost less than purchasing separate policies. The package includes business personal property coverage, loss of income coverage, and equipment breakdown protection.

Equipment breakdown coverage pays for damage to HVAC equipment, computers, and electrical systems. This protection is particularly valuable for businesses that rely on diagnostic equipment and computer systems.

Claim Prevention Strategies

Safety Training

Regular safety training reduces workers' compensation claims and liability exposures. Focus training on proper lifting techniques, electrical safety, and chemical handling procedures. Document all training to demonstrate your commitment to safety.

Quality Control

Implement quality control procedures to prevent professional liability claims. Use written work orders, maintain installation records, and follow manufacturer specifications. Quality control reduces the likelihood of system failures and customer complaints.

Customer Communication

Clear communication prevents misunderstandings that lead to claims. Provide written estimates, explain system limitations, and document change orders. Good communication builds customer relationships and reduces dispute risks.

Working with Insurance Professionals

Independent Agents

Independent agents represent multiple insurance carriers and can compare coverage options. They understand HVAC risks and can recommend appropriate coverage limits. Independent agents also provide ongoing service and claims assistance.

Industry Specialists

Some insurance carriers specialize in contractor coverage. These specialists understand HVAC risks and offer tailored coverage options. Industry specialists may provide risk management resources and safety training programs.

Regular Coverage Reviews

Insurance needs change as your business grows. Review coverage annually to ensure adequate limits and appropriate coverage types. Add new coverage as you expand services or enter new markets.

Risk Management Practices

Documentation

Maintain detailed records of installations, maintenance, and repairs. Documentation helps defend claims and demonstrates professional practices. Include photographs, material receipts, and customer communications in project files.

Vendor Relationships

Work with reputable suppliers and subcontractors who carry adequate insurance. Require certificates of insurance from subcontractors before starting work. Vendor relationships affect your liability exposures and insurance requirements.

Contract Review

Review contracts carefully before signing. Understanding your obligations helps prevent disputes and claims. Consider having an attorney review large or complex contracts to identify potential issues.

HVAC contractors face complex risks that require comprehensive insurance protection. The right coverage combination protects your business assets, meets regulatory requirements, and provides peace of mind. Work with experienced insurance professionals who understand your industry to develop an appropriate insurance program for your business needs.

HVAC Contractors Insurance Guide: Central Florida Edition

Central Florida's unique climate and building environment create specific challenges for HVAC contractors. High humidity levels, frequent severe weather, and year-round cooling demands increase both business opportunities and insurance risks. Understanding the coverage requirements for your Central Florida HVAC business ensures proper protection and regulatory compliance.

Central Florida HVAC Risk Factors

Hurricane and Severe Weather Exposure

Central Florida experiences frequent severe weather events including hurricanes, tornadoes, and severe thunderstorms. These events create emergency repair opportunities but also increase liability exposures. Your crews may work on damaged systems, unstable structures, and in hazardous conditions.

Commercial property insurance becomes critical for protecting your shop, warehouse, and equipment from wind and flood damage. Business interruption coverage helps maintain operations when severe weather forces temporary closures.

High Humidity Challenges

Central Florida's humidity creates unique HVAC system demands and potential failure modes. Condensation issues, mold growth, and indoor air quality problems occur more frequently. These conditions increase professional liability exposures when systems fail to control moisture properly.

Pollution liability insurance gains importance due to humidity-related issues. Mold contamination from faulty HVAC installations can result in significant cleanup costs and health claims.

Year-Round Operating Season

Unlike northern climates, Central Florida HVAC systems operate continuously. This creates more opportunities for system failures and emergency service calls. Continuous operation also increases wear on your equipment and vehicles.

Commercial auto insurance requires careful attention due to increased mileage and emergency response driving. Tools and equipment coverage becomes more valuable with constant field operations.

Essential Coverage for Central Florida HVAC Contractors

General Liability Insurance

General liability insurance protects against property damage and bodily injury claims from your work. Central Florida's building environment creates specific exposures including damage to tile floors common in the region, water damage from condensation issues, and injuries from equipment in tight spaces.

The policy should include completed operations coverage for claims arising after project completion. Humidity-related problems may not appear immediately, making this coverage essential for Central Florida contractors.

Workers' Compensation Insurance

Workers' compensation coverage is mandatory for Florida employers. The hot, humid conditions increase heat-related illness risks for technicians working in attics, crawl spaces, and on rooftops. Coverage includes medical treatment and lost wages for heat exhaustion, dehydration, and related injuries.

Consider enhanced coverage for emergency response work during severe weather events. Storm restoration creates additional injury risks that may exceed normal exposure levels.

Commercial Auto Insurance

Your fleet faces increased risks from Central Florida's traffic patterns, tourist activity, and severe weather. Commercial auto insurance should include comprehensive coverage for wind and flood damage. Emergency response driving during severe weather increases accident risks.

Consider higher liability limits due to the region's legal environment and potential for significant damages. Equipment coverage should reflect the value of diagnostic tools and specialized equipment transported in your vehicles.

Professional Liability Insurance

Central Florida's building codes and energy efficiency requirements create professional liability exposures. Customers expect energy-efficient systems that control humidity effectively. Professional liability coverage protects against claims when systems fail to meet performance expectations.

Indoor air quality has increased importance in Central Florida's climate. Professional liability insurance covers claims related to inadequate ventilation, humidity control failures, and mold-related problems.

Specialized Coverage Considerations

Hurricane and Windstorm Coverage

Standard commercial property policies may exclude windstorm damage or require separate deductibles. Ensure your property coverage includes hurricane protection for your business premises and stored equipment.

Consider business interruption coverage for hurricane-related closures. Extended power outages and evacuation orders can force business interruptions lasting days or weeks.

Flood Insurance

Central Florida faces flood risks from hurricanes, heavy rainfall, and storm surge. Standard commercial property policies exclude flood damage. Separate flood insurance through the National Flood Insurance Program or private carriers protects your business property.

Equipment Breakdown Coverage

Constant system operation and high humidity increase equipment breakdown risks. Equipment breakdown coverage pays for damage to your diagnostic equipment, computer systems, and shop machinery from power surges, mechanical failures, and electrical problems.

Regulatory and Licensing Requirements

Florida Contractor Licensing

Florida requires specific licenses for HVAC contractors. Class A licenses allow unrestricted HVAC work, while Class B and Class C licenses have monetary and scope limitations. All license classes require proof of general liability and workers' compensation insurance.

Maintain continuous coverage to avoid license suspension or revocation. The Florida Department of Business and Professional Regulation monitors insurance compliance for all licensed contractors.

EPA Certification Requirements

EPA certification for refrigerant handling is mandatory regardless of your location. Central Florida's year-round cooling season means constant refrigerant work. Proper certification helps prevent violations and maintains insurance coverage eligibility.

Local Permit Requirements

Central Florida municipalities may require additional permits and insurance for HVAC work. Hurricane mitigation work often requires enhanced coverage or bonding. Verify local requirements before starting projects in different jurisdictions.

Risk Management for Central Florida Operations

Heat Safety Protocols

Implement comprehensive heat safety protocols for outdoor work. Provide hydration stations, schedule frequent breaks, and monitor workers for heat stress symptoms. Heat-related workers' compensation claims are preventable with proper precautions.

Document safety training and maintain records of heat safety compliance. Insurance carriers may offer premium credits for documented safety programs.

Emergency Response Procedures

Develop procedures for storm response and emergency service calls. Enhanced safety protocols reduce injury risks during hazardous conditions. Consider limiting operations during severe weather warnings to protect employee safety.

Customer Communication

Clear communication about humidity control and system limitations prevents disputes. Document discussions about indoor air quality expectations and system performance parameters. Written communication helps defend professional liability claims.

Insurance Carrier Selection

Regional Experience

Choose insurance carriers with Central Florida experience. Regional carriers understand local risks, building practices, and legal environments. They may offer specialized coverage options for hurricane and humidity-related exposures.

Claims Handling

Evaluate carriers' hurricane claims handling capabilities. Severe weather events can overwhelm claims departments and delay settlements. Choose carriers with dedicated catastrophe response teams and local claims offices.

Safety Resources

Many carriers provide safety training and risk management resources. Take advantage of heat safety training, hurricane preparedness programs, and equipment maintenance guidance. These resources help prevent claims and may reduce insurance costs.

Building Your Insurance Program

Foundation Coverage

Start with a Business Owner's Policy combining general liability and property coverage. Add workers' compensation insurance if you employ technicians. Include commercial auto coverage for all business vehicles.

Enhanced Protection

Add professional liability insurance for design and consulting services. Include pollution liability coverage for refrigerant and chemical exposures. Consider cyber liability protection for customer data and business systems.

Catastrophe Protection

Ensure adequate hurricane and flood coverage for your business property. Include business interruption coverage for weather-related closures. Consider umbrella coverage for large commercial projects requiring higher liability limits.

Central Florida HVAC contractors face unique challenges requiring specialized insurance protection. The combination of severe weather risks, continuous operating demands, and regulatory requirements creates complex exposures. Working with experienced insurance professionals helps ensure adequate coverage for your Central Florida HVAC business.

Essential Insurance Coverage Guide for Residential Painters

Residential painting contractors face diverse risks that extend far beyond paint spills. You work with ladders, scaffolding, and chemicals while transforming customers' most valuable possessions. Property damage, injuries, and professional errors can result in significant financial losses. Comprehensive insurance coverage protects your business and provides the foundation for sustainable growth.

Core Insurance Requirements

General Liability Insurance

General liability insurance provides essential protection for residential painters. This coverage protects your business when your work causes property damage or bodily injury to others. Common claims include paint damage to customer property, injuries from slipping on drop cloths, and damage from moving furniture or equipment.

The policy covers legal defense costs, medical expenses, and property damage settlements. Completed operations coverage extends protection beyond the job site completion date. Paint failures, color disputes, or surface preparation issues discovered months later fall under completed operations protection.

Product liability coverage protects against claims related to defective paint, primers, or other materials you supply to customers. This protection becomes important when material failures cause property damage or health issues.

Workers' Compensation Insurance

Workers' compensation insurance is required for painting contractors who employ workers. Painting involves physical risks including ladder falls, chemical exposure, and repetitive motion injuries. Workers' compensation covers medical treatment and lost wages for injured employees.

The coverage also protects your business from employee lawsuits related to workplace injuries. Without workers' compensation, injured employees can sue your business for medical expenses, lost wages, and pain and suffering damages.

Commercial Auto Insurance

Painters transport equipment, materials, and crews between job sites daily. Commercial auto insurance covers your work vehicles, trailers, and equipment during transport. Personal auto policies exclude business use and provide no coverage for commercial activities.

The policy includes liability coverage for accidents involving your business vehicles. Physical damage coverage protects against theft, vandalism, and collision damage. Most commercial auto policies include limited coverage for tools and equipment stored in vehicles.

Specialized Coverage Options

Tools and Equipment Insurance

Painting equipment represents a significant investment requiring specialized protection. Tools and equipment coverage, also called inland marine insurance, protects your assets against theft and damage whether at job sites, in transit, or at your business premises.

Coverage includes spray equipment, ladders, scaffolding, sanders, and hand tools. The policy follows your equipment to customer properties and covers theft from vehicles or job sites. Standard business property policies typically exclude equipment used away from your premises.

Professional Liability Insurance

Professional liability insurance covers claims related to your professional advice and services. Color matching disputes, surface preparation recommendations, and coating selection advice create professional liability exposures. Customers may claim your recommendations were incorrect or your work failed to meet industry standards.

This coverage protects against claims of errors, omissions, or negligence in your professional services. Professional liability insurance covers legal defense costs and damages awarded against your business.

Pollution Liability Insurance

Standard general liability policies exclude pollution-related incidents. Painting contractors work with paints, solvents, and chemicals that can cause environmental contamination. Pollution liability insurance specifically covers these exposures.

The policy protects against costs from paint spills, solvent contamination, and chemical releases. Coverage includes cleanup expenses, third-party claims, and regulatory fines. Even small spills can result in significant cleanup costs and environmental liability.

Commercial Property Insurance

Commercial property insurance protects your business premises, inventory, and equipment stored at your location. Coverage includes paint inventory, office equipment, and furniture. Business personal property protection covers your assets against fire, theft, vandalism, and other covered perils.

Consider business interruption coverage to protect against lost income when covered events force business closures. Extended periods of downtime can threaten business survival without income replacement coverage.

Business Owner's Policy Advantages

A Business Owner's Policy (BOP) combines general liability and commercial property coverage in one comprehensive package. BOPs typically provide broader coverage at lower costs than purchasing separate policies. The package approach simplifies coverage management and policy administration.

Standard BOP coverage includes business personal property protection, loss of income coverage, and equipment breakdown protection. Many BOPs include limited cyber liability coverage for data breaches and system failures.

Risk Management Strategies

Safety Training and Protocols

Implement comprehensive safety training focusing on ladder safety, chemical handling, and fall protection. Regular training reduces workers' compensation claims and improves overall job site safety. Document all training to demonstrate your commitment to worker protection.

Establish protocols for scaffold setup, ladder positioning, and chemical storage. Safety protocols reduce injury risks and demonstrate professional practices to customers and insurance carriers.

Quality Control Procedures

Develop quality control procedures to prevent professional liability claims. Use written estimates, maintain detailed project specifications, and document surface preparation procedures. Quality control reduces customer disputes and claim frequencies.

Color approval processes prevent disputes over paint colors and finishes. Require customer sign-off on color samples and maintain documentation of all approvals.

Customer Communication

Clear communication prevents misunderstandings that lead to claims. Explain project scope, timeline expectations, and material limitations in writing. Good communication builds customer relationships and reduces dispute risks.

Document all change orders and additional work requests. Written documentation protects against claims for unauthorized work or billing disputes.

Contractor Licensing and Insurance

State Licensing Requirements

Most states require general liability insurance for painting contractor licenses. Verify specific requirements with your state licensing authority. Some jurisdictions require minimum coverage amounts or specific policy provisions.

Workers' compensation insurance is typically required for contractors with employees. Maintain continuous coverage to avoid license suspension or revocation.

Surety Bond Requirements

Some jurisdictions require surety bonds for painting contractor licensing. Bonds guarantee you will complete work according to contract terms and pay subcontractors and suppliers. Unlike insurance, bonds protect project owners rather than your business.

Consider voluntary bonding to demonstrate financial responsibility to customers. Bonded contractors often receive preference for larger residential projects.

Insurance Carrier Selection

Industry Experience

Choose insurance carriers with painting contractor experience. Specialized carriers understand industry risks and offer appropriate coverage options. They may provide safety resources, training programs, and risk management assistance.

Claims Handling

Evaluate carriers' claims handling reputation and local service capabilities. Prompt claims service maintains customer relationships and minimizes business disruption. Consider carriers with local claims offices for faster service.

Coverage Options

Compare coverage options including policy limits, deductibles, and exclusions. Some carriers offer specialized endorsements for painting contractors including pollution liability and professional liability coverage.

Working with Insurance Professionals

Independent Agents

Independent agents represent multiple carriers and can compare coverage options. They understand painting risks and can recommend appropriate protection for your business size and services.

Annual Reviews

Review your insurance program annually as your business grows. Add coverage for new services, increased equipment values, and higher revenue levels. Regular reviews ensure adequate protection for your evolving business needs.

Risk Management Resources

Take advantage of insurance carrier risk management resources. Many carriers provide safety training, contract review services, and loss control guidance. These resources help prevent claims and may qualify for premium discounts.

Building Your Insurance Foundation

Essential Coverage

Start with general liability insurance to meet licensing requirements and protect against common claims. Add workers' compensation if you employ painters or helpers. Include commercial auto coverage for all business vehicles.

Enhanced Protection

Consider professional liability insurance if you provide color consultation or surface preparation advice. Add tools and equipment coverage to protect your valuable assets. Include pollution liability coverage for chemical and paint exposures.

Growth Planning

Plan insurance coverage to support business growth. Consider umbrella coverage for large projects requiring higher liability limits. Cyber liability coverage becomes important as you use technology for customer management and billing.

Residential painting contractors face diverse risks requiring comprehensive insurance protection. The right coverage combination protects your business assets, meets regulatory requirements, and provides peace of mind for serving customers. Work with experienced insurance professionals to develop an appropriate program for your painting business.

Complete Insurance Guide for Flooring Installers

Flooring installation involves precision work with valuable materials in occupied buildings. You handle expensive hardwood, delicate tiles, and complex installation tools while working around furniture, electrical systems, and plumbing. Mistakes can result in significant property damage, customer disputes, and business-threatening liability claims. Proper insurance coverage protects your investment and ensures business continuity.

Essential Coverage Types

General Liability Insurance

General liability insurance forms the cornerstone of protection for flooring installers. This coverage protects your business when installation work causes property damage or bodily injury to others. Common scenarios include water damage from improper subfloor preparation, scratches to walls or furniture during material transport, and customer injuries from uneven transitions or installation debris.

The policy includes completed operations coverage extending protection after job completion. Flooring problems may not appear immediately after installation. Gaps, buckling, or adhesive failures discovered months later fall under completed operations protection.

Product liability coverage protects against claims related to defective flooring materials, adhesives, or installation products you supply to customers. When material failures cause property damage or safety hazards, product liability coverage provides essential protection.

Workers' Compensation Insurance

Workers' compensation insurance is mandatory for flooring contractors employing installation crews. Flooring installation involves significant physical demands including heavy lifting, kneeling, and repetitive motions. Common injuries include back strains, knee problems, and cuts from installation tools.

This coverage pays medical expenses and lost wages for employees injured during work. Workers' compensation also protects your business from employee lawsuits related to workplace injuries. The coverage includes rehabilitation services and disability benefits for serious injuries.

Commercial Auto Insurance

Flooring installers transport valuable materials and specialized equipment between job sites. Commercial auto insurance covers your work vehicles, trailers, and equipment during transport. Personal auto policies exclude business use and provide no protection for commercial operations.

The policy includes liability coverage for accidents involving business vehicles. Physical damage coverage protects against theft, vandalism, and collision damage. Commercial auto policies often include limited coverage for tools and materials stored in vehicles.

Tools and Equipment Coverage

Flooring installation requires specialized and expensive tools including saws, sanders, nailers, and measuring equipment. Tools and equipment coverage, also called inland marine insurance, protects these assets against theft and damage at job sites, in transit, or at your business location.

Standard business property policies typically exclude tools and equipment used away from your premises. Specialized coverage fills this gap and follows your equipment wherever work takes you.

Professional Protection

Professional Liability Insurance

Professional liability insurance covers claims related to your professional advice and installation services. Flooring installers provide recommendations on material selection, subfloor preparation, and installation methods. Professional liability protects against claims when your advice or installation methods fail to meet customer expectations.

Coverage includes errors in measuring, incorrect installation techniques, and inadequate surface preparation recommendations. Professional liability insurance covers legal defense costs and damages awarded against your business.

Pollution Liability Insurance

Standard general liability policies exclude pollution-related incidents. Flooring installers work with adhesives, sealers, and finishes that can cause environmental contamination. Pollution liability insurance specifically addresses these exposures.

The policy covers costs from adhesive spills, VOC emissions, and chemical contamination. Coverage includes cleanup expenses, third-party health claims, and regulatory penalties. Even minor spills can result in significant remediation costs.

Cyber Liability Insurance

Modern flooring businesses rely on technology for customer management, scheduling, and payment processing. Cyber liability insurance protects against data breaches, ransomware attacks, and system failures. Coverage includes notification costs, credit monitoring services, and business interruption losses.

Property and Business Protection

Commercial Property Insurance

Commercial property insurance protects your business premises, inventory, and equipment. Coverage includes flooring materials, office equipment, and tools stored at your location. Business personal property protection covers your assets against fire, theft, vandalism, and weather damage.

Business interruption coverage protects against lost income when covered events force business closures. Extended downtime can threaten business survival without income replacement protection.

Equipment Breakdown Coverage

Flooring installation relies on specialized equipment that can fail unexpectedly. Equipment breakdown coverage pays for repair or replacement of damaged sanders, saws, and other power equipment. Coverage includes electrical damage from power surges and mechanical breakdowns.

Business Owner's Policy Benefits

A Business Owner's Policy (BOP) combines general liability and commercial property coverage in one package. BOPs typically cost less than purchasing separate policies while providing comprehensive protection. The package includes business personal property coverage, loss of income protection, and equipment breakdown coverage.

Many BOPs include crime coverage for theft of money, securities, and business property. The comprehensive approach simplifies policy management and often provides broader coverage than individual policies.

Risk Management Practices

Installation Protocols

Develop standardized installation procedures to ensure consistent quality and reduce liability exposures. Document subfloor inspection procedures, material acclimation requirements, and installation specifications. Consistent protocols prevent problems that lead to customer claims.

Moisture testing procedures are critical for preventing flooring failures. Document all moisture readings and maintain records for future reference. Proper moisture control prevents warranty claims and professional liability issues.

Quality Control Measures

Implement quality control checkpoints throughout each installation. Pre-installation inspections identify potential problems before they become costly claims. Final inspections ensure customer satisfaction and identify any immediate concerns.

Maintain detailed installation records including photos, material specifications, and environmental conditions. Documentation helps defend claims and demonstrates professional practices.

Customer Communication

Clear communication prevents misunderstandings that lead to disputes. Explain installation processes, timeline expectations, and maintenance requirements in writing. Discuss limitations of different flooring materials and installation methods.

Document all change orders and additional work requests. Written communication protects against claims for unauthorized work or billing disputes.

Licensing and Regulatory Compliance

Contractor Licensing

Most jurisdictions require general liability insurance for flooring contractor licenses. Verify specific requirements with local licensing authorities. Some areas require minimum coverage amounts or specialized policy provisions.

Workers' compensation insurance is typically required for contractors with employees. Maintain continuous coverage to avoid license suspension or revocation.

Building Code Compliance

Flooring installations must comply with local building codes and accessibility requirements. Understand code requirements for different types of installations and maintain compliance documentation. Code violations can result in claims and regulatory penalties.

Manufacturer Warranty Requirements

Many flooring manufacturers require certified installers and specific installation procedures to maintain product warranties. Understand warranty requirements and maintain proper certifications to avoid warranty disputes.

Selecting Insurance Providers

Industry Specialization

Choose insurance carriers with flooring contractor experience. Specialized carriers understand industry risks and offer appropriate coverage options. They may provide risk management resources and safety training programs.

Claims Service

Evaluate carriers' claims handling capabilities and local service availability. Prompt claims service maintains customer relationships and minimizes business disruption. Consider carriers with experience handling flooring-related claims.

Coverage Flexibility

Compare coverage options including policy limits, deductibles, and available endorsements. Some carriers offer specialized coverage for flooring contractors including installation error protection and material coverage.

Building Your Insurance Program

Foundation Coverage

Begin with general liability insurance to meet licensing requirements and protect against common claims. Add workers' compensation insurance if you employ installation crews. Include commercial auto coverage for all business vehicles and equipment transport.

Specialized Protection

Consider professional liability insurance for design and specification services. Add tools and equipment coverage to protect valuable installation tools. Include pollution liability coverage for adhesive and chemical exposures.

Enhanced Coverage

Evaluate cyber liability insurance for customer data protection. Consider umbrella coverage for large commercial projects requiring higher liability limits. Equipment breakdown coverage protects against unexpected equipment failures.

Working with Insurance Professionals

Independent Agents

Independent agents represent multiple insurance carriers and can compare coverage options. They understand flooring risks and can recommend appropriate protection for your business size and specialties.

Regular Reviews

Review insurance coverage annually as your business evolves. Add coverage for new services, increased equipment values, and expanded operations. Regular reviews ensure adequate protection for changing business needs.

Risk Management Support

Take advantage of carrier risk management resources including safety training, loss control services, and contract review assistance. These resources help prevent claims and may qualify for premium reductions.

Flooring installers face complex risks requiring comprehensive insurance protection. The right coverage combination protects your business investment, ensures regulatory compliance, and provides confidence for serving customers. Partner with experienced insurance professionals to develop an appropriate program for your flooring installation business.

Insurance Essentials for General Contractors: Complete Coverage Guide

General contractors coordinate complex projects involving multiple trades, substantial financial investments, and significant liability exposures. You manage subcontractors, oversee construction timelines, and ensure project completion while navigating regulatory requirements and customer expectations. Comprehensive insurance coverage protects your business from the diverse risks inherent in construction management and provides the foundation for sustainable growth.

Core Insurance Protection

General Liability Insurance

General liability insurance provides fundamental protection for general contractors against property damage and bodily injury claims. Construction sites present numerous hazards including uneven surfaces, construction materials, and ongoing work activities. Common claims include injuries to visitors or passersby, damage to adjacent properties, and accidents involving construction equipment.

The policy includes completed operations coverage protecting against claims arising after project completion. Structural problems, water infiltration, or system failures discovered months or years later fall under completed operations protection. This coverage remains critical given the long-term nature of construction liability exposures.

Product liability coverage protects against claims related to defective materials or products you install or supply. When building components fail and cause property damage or injuries, product liability coverage provides essential protection.

Workers' Compensation Insurance

Workers' compensation insurance is mandatory for general contractors employing construction workers. Construction involves inherent risks including falls, equipment accidents, and injuries from tools and materials. Workers' compensation covers medical treatment and lost wages for injured employees.

The coverage also protects your business from employee lawsuits related to workplace injuries. Construction injuries can result in significant medical expenses and long-term disability claims. Workers' compensation provides defined benefits while protecting against unlimited liability exposure.

Commercial Auto Insurance

General contractors require commercial auto coverage for work vehicles, equipment transport, and job site mobility. Commercial auto insurance covers trucks, trailers, and specialized vehicles used for construction activities. Personal auto policies exclude business use and provide no protection for commercial operations.

The policy includes liability coverage for accidents involving business vehicles and equipment. Physical damage coverage protects against theft, vandalism, and collision damage. Commercial auto policies often include coverage for tools and equipment transported in vehicles.

Professional Services Protection

Professional Liability Insurance

Professional liability insurance covers claims related to your professional services including project management, design oversight, and construction administration. General contractors increasingly provide consulting services, value engineering, and project planning advice. Professional liability protects against claims of errors, omissions, or negligence in these services.

Coverage applies when customers claim your project management was inadequate, your recommendations caused problems, or your oversight failed to prevent issues. Professional liability insurance covers legal defense costs and damages awarded against your business.

Builders Risk Insurance

Builders risk insurance protects construction projects against property damage during construction. Coverage applies to the structure under construction, temporary structures, and materials stored on-site. Standard property policies exclude coverage for projects under construction.

The policy covers damage from fire, theft, vandalism, and weather events. Some policies include coverage for design errors, faulty workmanship, and materials storage off-site. Builders risk insurance typically covers the project until completion and acceptance by the owner.

Pollution Liability Insurance

Construction activities can result in environmental contamination requiring specialized coverage. Standard general liability policies exclude pollution-related incidents. Pollution liability insurance covers costs from fuel spills, asbestos disturbance, and contamination from construction activities.

Coverage includes cleanup expenses, third-party claims, and regulatory penalties. Even minor environmental incidents can result in significant remediation costs and regulatory fines.

Equipment and Tools Protection

Contractor's Equipment Coverage

General contractors invest heavily in equipment including excavators, cranes, and specialized construction machinery. Contractor's equipment coverage protects these assets against theft, damage, and breakdown whether on job sites, in transit, or at storage facilities.

The policy covers repair costs, replacement expenses, and rental costs for substitute equipment. Equipment breakdowns can delay projects and result in significant financial losses without proper coverage.

Tools Coverage

Construction tools represent substantial investments requiring specialized protection. Tools coverage protects hand tools, power tools, and surveying equipment against theft and damage. Coverage applies at job sites, in vehicles, and at storage locations.

Standard commercial property policies typically exclude tools used away from business premises. Specialized tools coverage fills this gap and follows your equipment to all work locations.

Business Protection Strategies

Commercial Property Insurance

Commercial property insurance protects your business premises, office equipment, and stored materials. Coverage includes office buildings, warehouses, and equipment storage facilities. Business personal property protection covers furniture, computers, and business records.

Business interruption coverage protects against lost income when covered events prevent business operations. Extended business interruptions can threaten contractor viability without income replacement protection.

Cyber Liability Insurance

Modern construction businesses rely on technology for project management, scheduling, and communication. Cyber liability insurance protects against data breaches, ransomware attacks, and system failures. Coverage includes notification costs, system restoration, and business interruption losses.

Surety Bonds

Many construction projects require surety bonds guaranteeing project completion and contractor performance. Performance bonds guarantee you will complete projects according to contract terms. Payment bonds guarantee payment to subcontractors and suppliers.

Unlike insurance, surety bonds protect project owners rather than your business. However, bonds demonstrate financial strength and enable participation in bonded projects requiring this protection.

Subcontractor Risk Management

Certificate of Insurance Requirements

Require certificates of insurance from all subcontractors before starting work. Verify that subcontractors carry adequate general liability, workers' compensation, and auto insurance. Missing or inadequate subcontractor coverage can create significant liability exposures for general contractors.

Additional Insured Coverage

Require subcontractors to name your business as an additional insured on their liability policies. Additional insured status provides coverage when subcontractor activities cause claims against your business. This protection is essential for managing subcontractor-related liability exposures.

Waiver of Subrogation

Consider requiring waivers of subrogation from subcontractors to prevent insurance carriers from pursuing recovery against your business for claims involving subcontractor activities. These waivers help prevent disputes between insurance carriers that can delay claim settlements.

Risk Management Practices

Safety Programs

Implement comprehensive safety programs focusing on fall protection, equipment operation, and hazard communication. Regular safety training reduces workers' compensation claims and improves overall job site safety. Document safety training and maintain records of compliance.

Establish job site safety protocols including personal protective equipment requirements, equipment inspection procedures, and emergency response plans. Safety programs demonstrate professional practices and may qualify for insurance premium discounts.

Quality Control

Develop quality control procedures to prevent construction defects and professional liability claims. Regular inspections identify problems before they become costly claims. Document all inspections and corrective actions taken.

Maintain detailed project records including change orders, material specifications, and inspection reports. Documentation helps defend claims and demonstrates professional project management practices.

Insurance Program Development

Business Owner's Policy

Consider a Business Owner's Policy (BOP) combining general liability and commercial property coverage. BOPs typically provide broader coverage at lower costs than separate policies. The package includes business personal property protection, loss of income coverage, and equipment breakdown protection.

Umbrella Coverage

Umbrella insurance provides additional liability coverage above primary policies. Large construction projects often require higher liability limits than standard policies provide. Umbrella coverage extends protection without purchasing separate high-limit policies.

Industry-Specific Carriers

Choose insurance carriers with construction industry experience. Specialized carriers understand contractor risks and offer appropriate coverage options. They may provide risk management resources, safety training programs, and claims expertise.

Regulatory Compliance

Licensing Requirements

Most jurisdictions require general liability and workers' compensation insurance for contractor licensing. Verify specific requirements with local licensing authorities. Some areas require minimum coverage amounts or bonding requirements.

Project Requirements

Review insurance requirements for each project before bidding. Owners often specify minimum coverage amounts, additional insured requirements, and waiver of subrogation provisions. Understanding requirements prevents surprises and ensures compliance.

Building Code Compliance

Maintain compliance with building codes and safety regulations throughout projects. Code violations can void insurance coverage and result in claims. Stay current with code changes and ensure subcontractor compliance.

General contractors face diverse and complex risks requiring comprehensive insurance protection. The right coverage combination protects your business investment, ensures regulatory compliance, and provides confidence for managing construction projects. Work with experienced insurance professionals who understand construction risks to develop an appropriate insurance program for your contracting business.

Cabinet Installers Insurance: Essential Coverage for Custom Installation Professionals

Cabinet installation combines precision craftsmanship with significant liability exposures. You work with expensive materials in occupied homes and commercial spaces while using power tools and handling heavy cabinetry. Installation errors can result in property damage, customer dissatisfaction, and costly warranty claims. Comprehensive insurance coverage protects your specialized business and ensures long-term success.

Primary Insurance Requirements

General Liability Insurance

General liability insurance provides essential protection for cabinet installers against property damage and bodily injury claims. Installation work creates numerous potential exposures including damage to walls, flooring, or plumbing during cabinet mounting, injuries from installation debris or tools, and water damage from incorrect connections to plumbing fixtures.

The policy includes completed operations coverage extending protection after installation completion. Cabinet problems may emerge months after installation including settling, hardware failures, or alignment issues. Completed operations coverage protects against these delayed claims.

Product liability coverage protects against claims related to defective cabinets, hardware, or installation materials you supply to customers. When cabinet components fail and cause property damage or injuries, this coverage provides essential protection.

Workers' Compensation Insurance

Workers' compensation insurance is mandatory for cabinet installers employing installation crews. Cabinet installation involves physical demands including heavy lifting, precise measuring, and power tool operation. Common injuries include back strains from lifting cabinets, cuts from installation tools, and injuries from falling objects.

This coverage pays medical expenses and lost wages for employees injured during work. Workers' compensation also protects your business from employee lawsuits related to workplace injuries and includes rehabilitation services for serious injuries.

Commercial Auto Insurance

Cabinet installers transport valuable products and installation tools between job sites. Commercial auto insurance covers work vehicles, trailers, and equipment during transport. Personal auto policies exclude business use and provide no coverage for commercial activities.

The policy includes liability coverage for accidents involving business vehicles and equipment. Physical damage coverage protects against theft, vandalism, and collision damage. Commercial auto policies often include limited coverage for cabinets and tools stored in vehicles.

Tools and Equipment Coverage

Cabinet installation requires specialized tools including routers, sanders, levels, and measuring equipment. Tools and equipment coverage, also called inland marine insurance, protects these assets against theft and damage at job sites, in transit, or at your workshop.

Coverage includes hand tools, power tools, and specialized installation equipment. Standard business property policies typically exclude tools and equipment used away from your premises, making specialized coverage essential for mobile installation operations.

Professional Services Protection

Professional Liability Insurance

Professional liability insurance covers claims related to your professional advice and installation services. Cabinet installers provide recommendations on cabinet selection, space planning, and installation methods. Professional liability protects against claims when your advice or installation fails to meet customer expectations.

Coverage includes errors in measuring, incorrect installation techniques, and inadequate space planning recommendations. Professional liability insurance covers legal defense costs and damages awarded against your business for professional errors or omissions.

Installation Errors Coverage

Some insurance carriers offer specialized coverage for installation errors beyond standard professional liability protection. This coverage addresses common cabinet installation problems including misaligned installations, incorrect measurements, and improper mounting that requires correction or replacement.

Pollution Liability Insurance

Cabinet installation involves adhesives, stains, and finishes that can cause environmental contamination. Standard general liability policies exclude pollution-related incidents. Pollution liability insurance specifically covers these exposures.

The policy covers costs from adhesive spills, VOC emissions from finishes, and chemical contamination. Coverage includes cleanup expenses, third-party health claims, and regulatory penalties for environmental violations.

Business Property Protection

Commercial Property Insurance

Commercial property insurance protects your workshop, showroom, and stored inventory. Coverage includes cabinet inventory, office equipment, and installation tools stored at your business location. Business personal property protection covers your assets against fire, theft, vandalism, and weather damage.

Consider business interruption coverage to protect against lost income when covered events prevent business operations. Extended downtime can threaten business survival without income replacement protection.

Bailee's Coverage

Cabinet installers often store customer-owned items during installation projects. Bailee's coverage protects customer property in your care, custody, or control against damage or theft. This coverage applies to existing cabinets removed during remodeling projects and customer belongings stored during installation.

Equipment Breakdown Coverage

Cabinet shops rely on specialized equipment including table saws, routers, and finishing equipment. Equipment breakdown coverage pays for repair or replacement of damaged equipment and covers electrical damage from power surges and mechanical breakdowns.

Risk Management Strategies

Installation Protocols

Develop standardized installation procedures to ensure consistent quality and reduce liability exposures. Document measurement procedures, mounting specifications, and quality control checkpoints. Consistent protocols prevent problems that lead to customer claims and warranty issues.

Pre-installation inspections identify potential problems before they become costly claims. Document wall conditions, plumbing locations, and electrical considerations that may affect installation success.

Quality Control Measures

Implement quality control checkpoints throughout each installation project. Template verification prevents measurement errors that require cabinet modification or replacement. Final inspections ensure customer satisfaction and identify any immediate concerns.

Maintain detailed installation records including photos, measurements, and any modifications made during installation. Documentation helps defend claims and demonstrates professional installation practices.

Customer Communication

Clear communication prevents misunderstandings that lead to disputes. Explain installation processes, timeline expectations, and potential complications in writing. Discuss cabinet limitations and maintenance requirements with customers.

Document all change orders and additional work requests. Written communication protects against claims for unauthorized work or billing disputes that can arise during complex remodeling projects.

Licensing and Compliance

Contractor Licensing

Most jurisdictions require general liability insurance for cabinet installation contractor licenses. Some areas classify cabinet installation under general contractor or specialty contractor licensing requirements. Verify specific requirements with local licensing authorities.

Workers' compensation insurance is typically required for contractors with employees. Maintain continuous coverage to avoid license suspension or revocation that can interrupt business operations.

Building Code Compliance

Cabinet installations must comply with local building codes and accessibility requirements. Understand code requirements for different installation types including ADA compliance for commercial projects. Code violations can result in claims and regulatory penalties.

Manufacturer Requirements

Many cabinet manufacturers require certified installers to maintain product warranties. Understand certification requirements and maintain proper training to avoid warranty disputes. Manufacturer requirements may affect your professional liability exposures.

Business Development Support

Bonding Capabilities

Some commercial projects require surety bonding for cabinet installation work. Establish bonding capabilities to demonstrate financial responsibility and qualify for larger projects. Bonds guarantee project completion and payment to suppliers.

Insurance Requirements

Commercial customers often specify minimum insurance requirements in installation contracts. Common requirements include specific liability limits, additional insured endorsements, and waiver of subrogation provisions. Understanding these requirements helps in project bidding and contract negotiations.

Insurance Provider Selection

Industry Experience

Choose insurance carriers with cabinet installer experience or general contractor specialization. Specialized carriers understand installation risks and offer appropriate coverage options. They may provide risk management resources and safety training programs.

Claims Handling

Evaluate carriers' claims handling capabilities and local service availability. Cabinet installation claims often involve customer satisfaction issues requiring sensitive handling. Consider carriers with experience in residential contractor claims.

Coverage Flexibility

Compare coverage options including policy limits, deductibles, and available endorsements. Some carriers offer package policies combining multiple coverage types while others prefer separate policy approaches.

Building Your Insurance Program

Foundation Coverage

Start with general liability insurance to meet licensing requirements and protect against common installation claims. Add workers' compensation insurance if you employ installation crews. Include commercial auto coverage for vehicles and equipment transport.

Specialized Protection

Consider professional liability insurance for design and planning services. Add tools and equipment coverage to protect valuable installation equipment. Include pollution liability coverage for adhesive and finishing exposures.

Enhanced Coverage

Evaluate business interruption coverage for workshop protection. Consider umbrella coverage for large commercial projects requiring higher liability limits. Cyber liability coverage protects customer information and business systems.

Professional Support

Independent Agents

Independent agents represent multiple insurance carriers and can compare coverage options for cabinet installers. They understand specialty contractor risks and can recommend appropriate protection for your business size and services.

Annual Reviews

Review insurance coverage annually as your business evolves and grows. Add coverage for new services, increased equipment values, and expanded operations. Regular reviews ensure adequate protection for changing business needs and market conditions.

Cabinet installers face unique risks requiring specialized insurance protection. The right coverage combination protects your craftsmanship investment, ensures regulatory compliance, and provides confidence for serving customers. Work with experienced insurance professionals who understand specialty contractor risks to develop appropriate coverage for your cabinet installation business.

Electrical Contractors Insurance: Complete Protection Guide for Licensed Electricians

Electrical contractors face some of the highest risk exposures in the construction industry. You work with potentially deadly electrical systems while installing, maintaining, and repairing infrastructure that affects entire buildings. Electrical fires, electrocution hazards, and system failures can result in catastrophic property damage, serious injuries, and substantial liability claims. Comprehensive insurance coverage protects your business and provides the foundation for professional electrical contracting.

Essential Coverage Requirements

General Liability Insurance

General liability insurance provides fundamental protection for electrical contractors against property damage and bodily injury claims. Electrical work creates significant exposures including electrical fires from faulty installations, electrocution injuries to workers or bystanders, and power outages affecting customer operations.

The policy includes completed operations coverage protecting against claims arising after project completion. Electrical system problems may not appear immediately but can cause fires, equipment damage, or operational failures months later. Completed operations coverage remains essential given the long-term nature of electrical system reliability.

Product liability coverage protects against claims related to defective electrical components, equipment, or materials you install. When electrical products fail and cause property damage or injuries, product liability coverage provides critical protection for your business.

Workers' Compensation Insurance

Workers' compensation insurance is mandatory for electrical contractors employing technicians and apprentices. Electrical work involves extreme hazards including electrocution risks, falls from elevated work areas, and injuries from electrical equipment. Workers' compensation covers medical treatment and lost wages for injured employees.

The coverage protects your business from employee lawsuits related to workplace injuries and includes rehabilitation services and disability benefits. Electrical injuries can be severe and result in long-term medical treatment making adequate workers' compensation coverage essential.

Commercial Auto Insurance

Electrical contractors require commercial auto coverage for service vehicles, equipment transport, and emergency response capabilities. Commercial auto insurance covers trucks, vans, and trailers used for electrical work. Personal auto policies exclude business use and provide no protection for commercial operations.

The policy includes liability coverage for accidents involving business vehicles and equipment. Physical damage coverage protects against theft, vandalism, and collision damage. Commercial auto policies often include coverage for tools and electrical materials transported in vehicles.

Professional Liability Insurance

Professional liability insurance covers claims related to your professional electrical services and advice. Electrical contractors provide system design recommendations, code compliance guidance, and electrical planning services. Professional liability protects against claims of errors, omissions, or negligence in these professional services.

Coverage applies when customers claim your electrical design was inadequate, your code interpretation was incorrect, or your recommendations caused system problems. Professional liability insurance covers legal defense costs and damages awarded against your business.

Specialized Electrical Coverage

Pollution Liability Insurance

Electrical work can result in environmental contamination requiring specialized coverage. PCB contamination from old electrical equipment, transformer oil spills, and hazardous material exposure during electrical system upgrades create pollution liability exposures.

Standard general liability policies exclude pollution-related incidents. Pollution liability insurance covers cleanup costs, third-party claims, and regulatory penalties for environmental contamination from electrical work.

Cyber Liability Insurance

Modern electrical systems include smart building technology, security systems, and network infrastructure. Electrical contractors increasingly work with cyber-physical systems requiring cyber liability protection. Coverage includes data breaches, system failures, and cyber attacks affecting customer systems.

Equipment Coverage

Electrical contractors invest heavily in specialized tools including multimeters, oscilloscopes, wire pulling equipment, and testing instruments. Equipment coverage protects these valuable assets against theft, damage, and breakdown whether at job sites, in vehicles, or at your shop.

The policy covers diagnostic equipment, hand tools, power tools, and vehicle-mounted equipment. Standard commercial property policies typically exclude equipment used away from business premises making specialized coverage essential.

Business Protection Strategies

Commercial Property Insurance

Commercial property insurance protects your business premises, inventory, and stored equipment. Coverage includes electrical supply inventory, office equipment, and tools stored at your location. Business personal property protection covers your assets against fire, theft, vandalism, and weather damage.

Business interruption coverage protects against lost income when covered events prevent business operations. Electrical contractors depend on continuous operations for emergency service contracts and project commitments.

Umbrella Insurance

Umbrella insurance provides additional liability coverage above primary policies. Large electrical projects often require higher liability limits than standard policies provide. Electrical system failures can cause significant property damage requiring substantial liability protection.

Surety Bonds

Many electrical projects require surety bonds guaranteeing contractor performance and code compliance. Performance bonds guarantee project completion while license bonds guarantee compliance with electrical codes and regulations.

Consider voluntary bonding to demonstrate financial responsibility and qualify for larger commercial projects requiring bonded contractors.

Risk Management Practices

Safety Programs

Implement comprehensive electrical safety programs focusing on lockout/tagout procedures, arc flash protection, and electrical hazard identification. Regular safety training reduces workers' compensation claims and prevents serious electrical accidents.

Establish protocols for electrical testing, personal protective equipment use, and emergency response procedures. Safety programs demonstrate professional practices and may qualify for insurance premium discounts.

Code Compliance

Maintain current knowledge of National Electrical Code requirements and local amendments. Code compliance prevents violations that can void insurance coverage and result in regulatory penalties. Document code compliance for all installations and repairs.

Quality Control

Develop quality control procedures to prevent electrical system failures and professional liability claims. Regular inspections and testing identify problems before they cause customer claims or safety hazards.

Maintain detailed installation records including electrical drawings, test results, and inspection reports. Documentation helps defend claims and demonstrates professional electrical practices.

Licensing and Regulatory Compliance

Electrical License Requirements

Electrical contractor licenses require proof of general liability and workers' compensation insurance. Master electrician licenses may have additional insurance requirements. Maintain continuous coverage to avoid license suspension or revocation.

Code Authority Requirements

Local code authorities may require specific insurance coverage for electrical permits and inspections. Some jurisdictions require pollution liability coverage for electrical work involving environmental hazards.

Customer Requirements

Commercial and industrial customers often specify minimum insurance requirements for electrical contractors. Common requirements include specific liability limits, additional insured endorsements, and electrical-specific coverage provisions.

Emergency Service Considerations

24/7 Operations

Many electrical contractors provide emergency services requiring around-the-clock operations. Emergency response increases liability exposures and requires adequate insurance coverage for elevated risk activities.

Critical Systems

Electrical work on hospitals, data centers, and emergency services requires enhanced liability protection. These facilities cannot tolerate electrical failures making professional liability coverage especially important.

Insurance Program Development

Business Owner's Policy

Consider a Business Owner's Policy (BOP) combining general liability and commercial property coverage. BOPs typically provide broader coverage at lower costs than separate policies for smaller electrical contracting operations.

Package Policies

Some insurers offer contractor package policies specifically designed for electrical contractors. These packages include general liability, professional liability, and equipment coverage tailored for electrical risks.

Industry Specialists

Choose insurance carriers with electrical contractor experience. Specialized carriers understand electrical risks and offer appropriate coverage options including electrical-specific endorsements and risk management resources.

Working with Insurance Professionals

Independent Agents

Independent agents represent multiple insurance carriers and can compare coverage options for electrical contractors. They understand electrical industry risks and can recommend appropriate protection for your business size and specialties.

Risk Management Support

Take advantage of insurance carrier risk management resources including electrical safety training, code compliance assistance, and loss control services. These resources help prevent claims and may qualify for premium reductions.

Annual Reviews

Review insurance coverage annually as electrical technology evolves and your business grows. Add coverage for new services like renewable energy systems, smart building technology, and energy storage installations.

Building Comprehensive Protection

Foundation Coverage

Start with general liability insurance meeting licensing requirements and protecting against electrical-related claims. Add workers' compensation for employees and commercial auto coverage for all business vehicles and equipment transport.

Professional Protection

Include professional liability insurance for electrical design and consulting services. Add pollution liability coverage for environmental exposures and cyber liability protection for smart building systems.

Equipment Protection

Secure comprehensive equipment coverage protecting valuable electrical tools and testing equipment. Consider business interruption coverage for income protection during equipment repairs or replacement.

Electrical contractors face unique and severe risks requiring specialized insurance protection. The right coverage combination protects your business investment, ensures regulatory compliance, and provides confidence for serving customers safely. Partner with experienced insurance professionals who understand electrical contractor risks to develop appropriate coverage for your electrical contracting business.

Coffee Shop Insurance: Essential Coverage for Your Café Business

Coffee shops create inviting spaces where customers gather, work, and socialize while enjoying hot beverages and food. Your business faces unique risks including hot beverage burns, slip and fall accidents, equipment failures, and food-related liabilities. The combination of customer interaction, food service, and specialized equipment requires comprehensive insurance coverage to protect your investment and ensure business continuity.

Core Insurance Protection

General Liability Insurance

General liability insurance provides essential protection for coffee shops against customer injuries and property damage claims. Common exposures include burns from hot coffee or espresso, slip and fall accidents on wet floors, and injuries from furniture or equipment. Customer injuries in coffee shops can result in significant medical expenses and liability claims.

The policy includes product liability coverage protecting against claims related to food poisoning, allergic reactions, or contaminated beverages. Coffee shops serving food items face additional exposures requiring comprehensive product liability protection.

Premises liability coverage protects against injuries occurring on your property including parking areas, sidewalks, and outdoor seating areas. This coverage is essential for coffee shops with drive-through service or outdoor dining options.

Workers' Compensation Insurance

Workers' compensation insurance is mandatory for coffee shops employing baristas, managers, and support staff. Coffee shop employees face risks including burns from hot equipment, cuts from coffee equipment, and repetitive motion injuries from espresso machine operation.

This coverage pays medical expenses and lost wages for employees injured during work. Workers' compensation also protects your business from employee lawsuits related to workplace injuries and includes rehabilitation services for serious injuries.

Commercial Property Insurance

Commercial property insurance protects your coffee shop premises, equipment, and inventory. Coverage includes espresso machines, grinders, brewing equipment, and furniture. Business personal property protection covers your assets against fire, theft, vandalism, and weather damage.

Consider business interruption coverage to protect against lost income when covered events prevent business operations. Coffee shops depend on daily operations and regular customer traffic making income protection essential.

Equipment Breakdown Coverage

Coffee shops rely heavily on specialized equipment including espresso machines, grinders, refrigeration units, and point-of-sale systems. Equipment breakdown coverage pays for repair or replacement of damaged equipment from mechanical failures, electrical problems, and power surges.

Coverage includes rental equipment costs while permanent repairs are completed. Equipment failures can force business closures making prompt replacement essential for maintaining operations.

Food Service Protection

Product Liability Insurance