Coffee Shop Insurance Guide: Brew a Safer Business

- marketing676641

- Oct 17, 2025

- 5 min read

Running a coffee shop requires more than perfecting your espresso blend. You need comprehensive insurance protection designed specifically for food service businesses. Coffee shop insurance protects against the unique risks of serving beverages and food in a public environment.

Your coffee shop faces daily exposure to customer injuries, equipment failures, product liability claims, and property damage. Without proper coverage, a single incident could close your doors permanently. Learn how the right insurance policies protect your investment and keep your business operational.

Essential Foundation: Business Owner's Policy (BOP)

A Business Owner's Policy combines general liability and property insurance at a lower cost than purchasing separate policies. BOPs typically include business interruption coverage, making them ideal for coffee shops operating on tight margins.

Property coverage within your BOP protects your espresso machines, grinders, furniture, inventory, and building improvements. This coverage extends to exterior elements like patios, umbrellas, and signage that enhance your customer experience.

General liability protection handles third-party injury and property damage claims. When customers slip on wet floors or suffer burns from hot beverages, your BOP responds with legal defense and settlement funds.

Business interruption coverage replaces lost income when covered disasters force temporary closure. If equipment failure or property damage shuts down operations, this coverage pays ongoing expenses and lost profits during repairs.

Property Insurance: Protecting Your Physical Assets

Commercial property insurance covers your building, equipment, inventory, and business personal property against fire, theft, vandalism, and weather damage. Coffee shops require specialized equipment coverage for expensive espresso machines, grinders, and brewing systems.

Equipment breakdown coverage protects against mechanical failures of essential equipment. When your main espresso machine breaks down during peak hours, this coverage pays for repairs and lost income from the interruption.

Your property policy should cover both interior and exterior assets including outdoor seating areas, drive-through equipment, and security systems. Many policies also cover spoilage of perishable inventory following equipment failures or power outages.

Consider replacement cost coverage rather than actual cash value. This ensures you can replace damaged equipment with new items rather than receiving depreciated values that may not cover full replacement costs.

General Liability: Customer Protection Coverage

General liability insurance provides essential protection against customer injury claims, product liability, and property damage lawsuits. Coffee shops face constant exposure to slip-and-fall accidents, burns from hot beverages, and food poisoning claims.

Product liability coverage handles claims when your food or beverages cause illness or injury. This protection covers legal defense costs, medical expenses, and settlements related to contaminated products or allergic reactions.

Customer property damage coverage responds when accidents damage customer belongings. Spilled coffee on laptops, stained clothing, or damaged phones create liability exposures that general liability insurance addresses.

Your policy also covers advertising injury claims related to copyright infringement, false advertising, or privacy violations in your marketing materials.

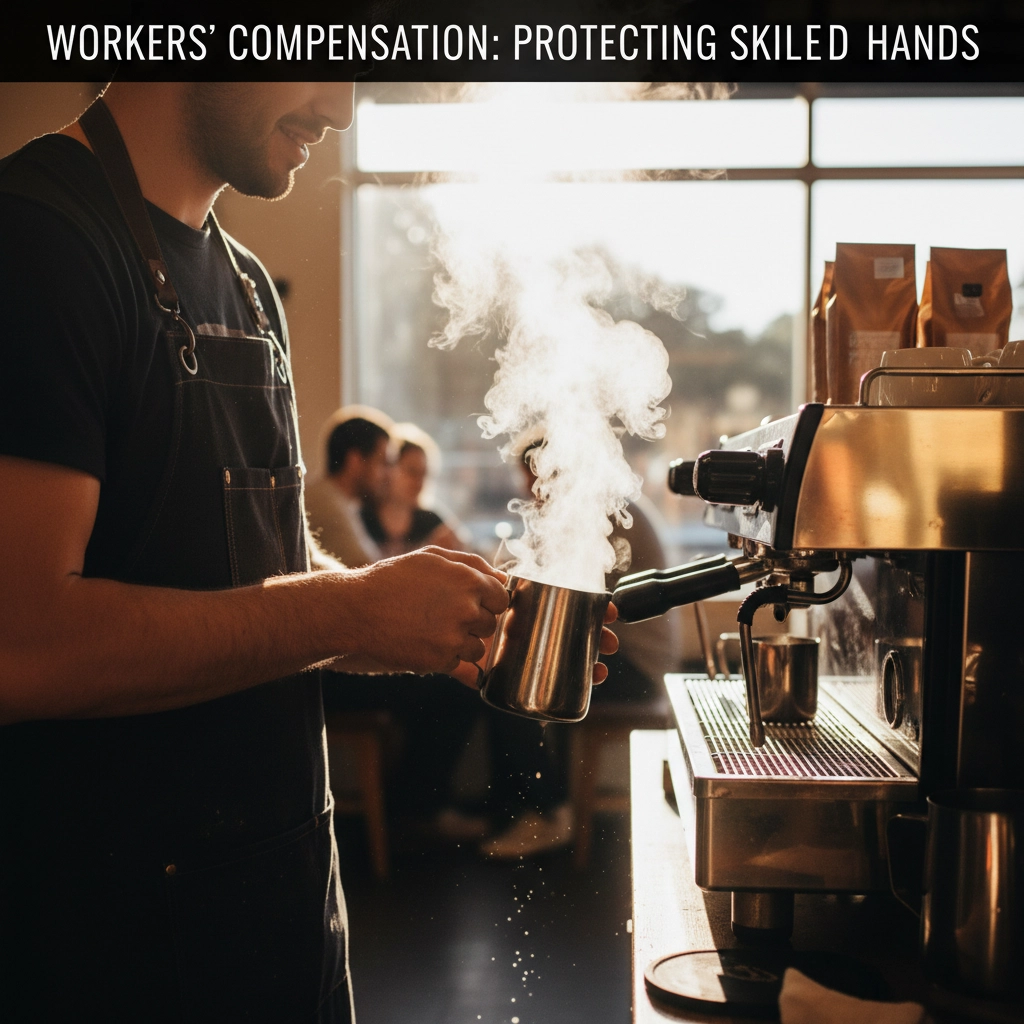

Workers' Compensation: Employee Protection

Workers' compensation insurance is mandatory in most states for businesses with employees. Coffee shops present numerous workplace injury risks including burns from hot equipment, cuts from cleaning tasks, and slips on wet surfaces.

This coverage pays medical expenses and lost wages for employees injured while working. It also provides disability benefits for workers unable to return to their previous duties due to work-related injuries.

Workers' compensation protects your business from employee lawsuits related to workplace injuries. Without this coverage, injured employees can sue your business directly for medical costs and damages.

The policy also covers occupational illnesses that develop over time from workplace exposures. Repetitive stress injuries and respiratory problems from cleaning chemicals qualify for coverage.

Commercial Auto Insurance: Vehicle Protection

Commercial auto insurance becomes necessary when your coffee shop owns delivery vehicles, catering vans, or company cars. Personal auto policies exclude business use, leaving you without coverage during commercial activities.

This coverage protects against liability claims, property damage, and injuries resulting from vehicle accidents during business operations. Delivery drivers and catering services create significant auto liability exposures.

If employees use personal vehicles for business purposes like bank deposits or supply runs, you need hired and non-owned auto coverage. This protects your business when employee-owned vehicles are involved in accidents during work activities.

Commercial auto policies also cover cargo and equipment transported in your vehicles. Catering supplies, equipment, and inventory receive protection against theft and damage during transport.

Additional Coverage Considerations

Cyber liability insurance protects against data breaches, ransomware attacks, and payment card fraud. Modern coffee shops rely on point-of-sale systems, customer databases, and wireless networks that create cyber security vulnerabilities.

Employment practices liability insurance (EPLI) covers discrimination, harassment, and wrongful termination claims. Food service businesses face higher employment lawsuit risks due to diverse workforces and high turnover rates.

Business income coverage extends beyond basic interruption insurance to cover income losses from various scenarios. Supply chain disruptions, utility outages, and nearby disasters can reduce customer traffic without directly damaging your property.

Crime insurance protects against employee theft, robbery, and fraud. Coffee shops handle significant cash transactions and maintain valuable inventory that attracts criminal activity.

Risk Management Strategies

Implement comprehensive safety protocols to reduce insurance claims and premiums. Regular equipment maintenance, employee training, and customer area inspections prevent many common accidents.

Maintain detailed incident reports for all accidents and near-misses. Documentation helps with insurance claims and identifies patterns that require additional safety measures.

Work with experienced food service insurance agents who understand coffee shop operations. Specialized agents identify coverage gaps and recommend appropriate limits based on your specific risks.

Review your coverage annually as your business grows and changes. New locations, expanded services, and increased revenues require coverage adjustments to maintain adequate protection.

Coverage Limits and Costs

Coffee shop insurance costs vary based on location, size, revenue, and claims history. General liability insurance typically ranges from $250 to $640 annually for basic coverage limits.

Business Owner's Policies cost between $500 and $980 annually, providing better value than separate policies. Higher coverage limits and additional endorsements increase premiums but provide better protection.

Workers' compensation costs depend on payroll amounts and job classifications. Food service workers generally have moderate risk ratings, but costs increase with higher payrolls and claim frequencies.

Consider umbrella liability coverage for additional protection beyond primary policy limits. This coverage provides excess liability protection at relatively low costs for catastrophic claims.

Choosing the Right Insurance Partner

Select insurance providers with food service industry experience and strong claims handling reputations. Quick claim processing and knowledgeable adjusters minimize business interruptions following losses.

Compare coverage features rather than just premiums when evaluating policies. Higher limits, broader coverage, and valuable endorsements often justify slightly higher premiums.

Look for insurance companies offering risk management resources, safety training, and loss control services. These value-added services help prevent claims and reduce long-term insurance costs.

Maintain continuous coverage without gaps to qualify for better rates and avoid coverage restrictions. Insurance companies reward long-term customers with stable coverage histories.

Coffee shop insurance protects your investment against the numerous risks of food service operations. Comprehensive coverage ensures your business survives unexpected events and continues serving your community. Contact Insurance Alliance LLC to discuss your coffee shop insurance needs and develop a protection plan tailored to your specific operations.

Comments